According to a new report published by Allied Market Research, titled, Luxury Apparels Market by Material, Gender, and Mode of Sale: Global Opportunity Analysis and Industry Forecast, 2017-2023,the luxury apparels market size was valued at $62.62 billion in 2016, and is projected to reach $81.23 billion by 2023, growing at a CAGR of 3.9% from 2017 to 2023. Cotton, one of the widely-worn materials, dominated the global market and is expected to maintain this trend till 2023. However, Asia-Pacific is expected to dominate the market throughout the forecast period due to rapid increase in urbanization and rise in disposable income.

Growth in online mode of sale, rapid urbanization, and change in lifestyle, owing to increased disposable income of the consumers, drive the luxury apparels market growth. In addition, growth in the emerging economies, such as Asia-Pacific and LAMEA, is anticipated to create lucrative opportunities for the global luxury apparels market. However, high cost of raw materials hampers the luxury apparels market growth.

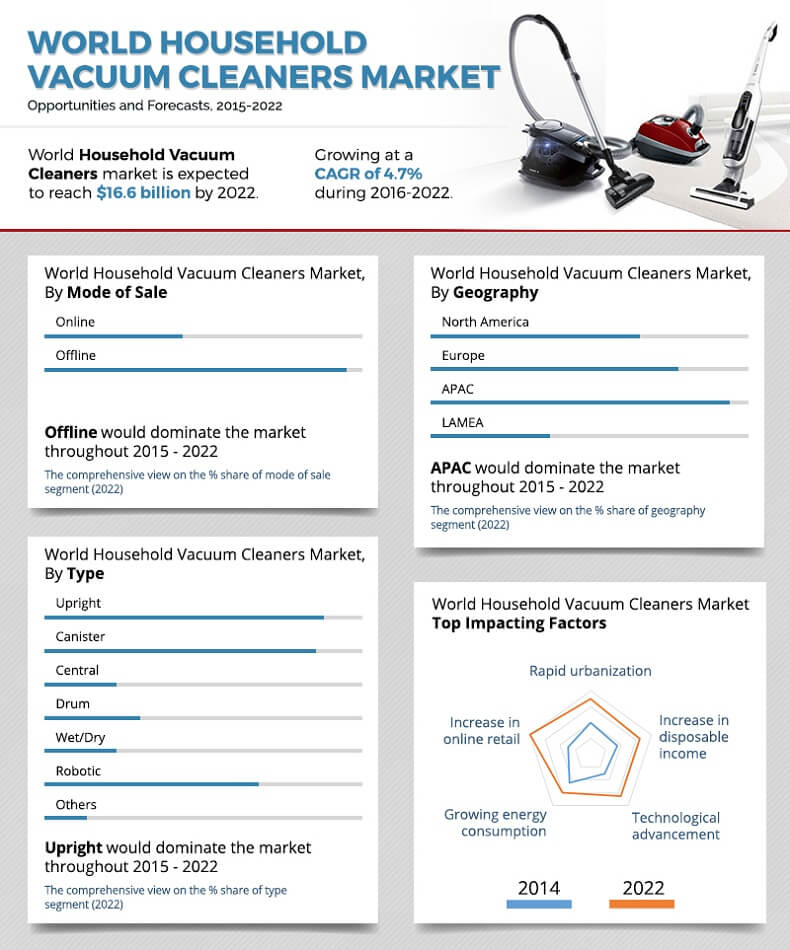

Download Sample Report: https://www.alliedmarketresearch.com/request-sample/2282

Leather is the second highest growing material in luxury apparels market during the forecast period, and is expected to exhibit a growth of 4.6% by 2023. Fashion-conscious consumers are getting increasingly sensible of the environment and thus, prefer eco-friendly apparel fabric products, which further promotes harmless and non-toxic production method of leather. Moreover, some of the consumers from BRICS (Brazil, Russia, India, China, and South Africa) are ready to pay higher prices for environmental-friendly fabric in which toxic and harmful dyes are not included. Some of the manufacturers in luxury apparels market, such as LVMH Moet Hennessy Louis Vuitton SA, Coach, Inc., Kering SA, Prada S.p.A, and Hermes International SCA, are involved innovating leather apparels and other goods using eco-friendly fabric material, thereby reducing the emission of pollutants and conserving the environment.

The market for denim is expected to drive with strong growth of denim production in Asia-Pacific, such as India, China, Pakistan, and others. The availability of cheap labor in Asia-Pacific is expected to contribute toward excess denim production, thereby supplementing the luxury denim market growth. In addition, advances in the denim industry have attracted customer base. For instance, the initiation of Lycra hybrid technology in the industry has gained popularity due to its super stretch properties. The blend of Lycra with denim has made denim more stretchable than the conventional stuff allowing customers to choose from a variety of options.

Denim is the most worn fabric apparel among global consumers and offers a wide range of products than other materials. Apparels, such as denim jackets, jeans, dresses, shirts, shorts, skirts, and tops, are some of the popular and preferred denim apparels used as regular wear. Moreover, unique weaving pattern of raw denim showcase it as a luxury apparel.

For Purchase Enquiry: https://www.alliedmarketresearch.com/purchase-enquiry/2282

Online sales in luxury apparels industry are expected to grow at the highest rate by 2023. E-commerce sales have gained popularity from the past years as online shopping offers a platform for easy shopping to the large customer base. The consumers are well informed about the garments fabric, size, and color code from the pictures and photos posted on the companys website or an e-commerce site. It has been observed that small-town customers have been contributing to the online sales due to lack of accessibility of authentic luxury apparels in the nearby stores, creating lucrative opportunities for the manufacturers to widen their regional base.

Europe accounted for the highest market share in luxury apparels market in 2016, and is expected to maintain its lead throughout the forecast period, owing to majority of the top luxury apparels manufacturers headquartered in UK, Italy, France, and Switzerland. LAMEA exhibited significant growth, owing to improvement in the purchasing parity, better standard of living, and availability of wide options.

Key Findings of the Luxury Apparels Market:

- In 2016, cotton material accounted for the maximum market revenue, and is projected to grow at a CAGR of 3.1 % during the forecast period.

- E-commerce sales are expected to grow at a significant CAGR of 5.6%, as it is a convenient way of shopping.

- The female consumers segment accounted for more than half of the global luxury apparels market in 2016.

- China is the major shareholder in the Asia-Pacific luxury apparels industry, and accounted for around 42.4% share in 2016.

The key players in luxury apparels market focus to expand their business operations in the emerging countries by adopting various strategies, such as acquisition and contact/agreement. The major players profiled in this report include Ralph Lauren Corporation, Christian Dior, Michael Kors, Coach, Inc., Gianni Versace S.P.A., Girogio Armani S.P.A., Nike, Inc., Hermes International, Inc., Tommy Hilfiger USA Inc., and Burberry Group, Inc.